Filling Holes in Safety Nets

26-08-2023

11:39 AM

1 min read

Why in News?

- The article highlights the revised G20/OECD draft of the 2011 High-level Principles on Financial Consumer Protection (FCP) and new themes that have been endorsed for the first time for FCP.

- It put emphasis that India must lead others by example and adopts the revised principles as it takes over G20 presidency in December 2023.

About Financial consumer protection (FCP)

- It refers to the general framework of laws, regulations, and other measures aimed at ensuring fair and responsible treatment of financial consumers in their purchases and usage of financial products and services, as well as their interactions with financial service providers.

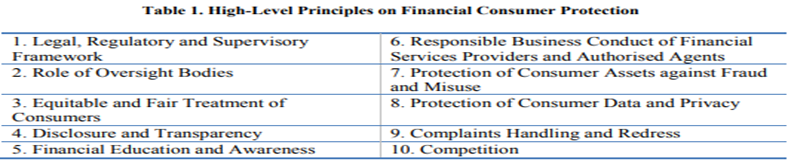

About G20/OECD High-Level Principles on FCP

- Background: These were developed as part of the Organisation for Economic Co-operation and Development’s (OECD) strategic response to the global financial crisis to enhance financial consumer protection.

- These Principles were endorsed by G20 Leaders in 2011 and adopted by the OECD Council in 2012 and are also included in the Financial Stability Board (“FSB”) Compendium of Standards.

- Applicability: As a high-level standard, these Principles are specifically designed and intended to be applicable to any jurisdiction and are cross-sectoral in nature (i.e. they can be applied to credit, banking, payments, insurance, pensions and investment sectors).

- Significance: The Principles are the leading international standard for effective and comprehensive financial consumer protection

Updating FCP principles

- Need: The proposed revisions to the FCP Principles in 2022 reflect developments such as the impact, opportunities and risks for consumers associated with digitalization, sustainable finance, financial well-being, as well as the lessons learnt from responding to the COVID-19 pandemic.

- Themes: These principles deal with three cross-cutting themes namely financial well-being, digitalization and sustainable finance.

- New Principles: Also in 2022, two additional principles were included, namely access and inclusion and quality financial products.

- Recommendations:

- Regulatory oversight: The updated principles also recommend intervention by regulators in certain high-risk products, cultivating appropriate firm culture and using behavioural insights to better consumer outcomes.

- Protection of vulnerable consumers: The new FCP regime calls for incorporating lessons and policy implications arising from the experience of the COVID-19 pandemic as appropriate, for example, including references to vulnerable consumers and financial scams.

Significance of financial well-being in updated FCP

- About financial well-being: It refers to being in control, feeling secure and having freedom about one’s own current and future finances.

- Financial well-being in ideal FCP regime: The FCP policies must contribute to overall financial well-being and resilience of consumers and must ensure adequate and easy to understand disclosures to consumers.

- How financial well-being can be achieved?

- By setting responsibility of service providers: Financial services providers should provide clear, accurate, reliable, comparable, easily accessible, and timely written information on the financial products and services being offered

- Standardised precontractual disclosure practices should be adopted, which enables comparison between products and services of the same nature.

- Oversight approach: This should aim to realise the potential benefits to financial consumers from innovative business approaches and maintain an appropriate degree of financial consumer protection.

- By setting responsibility of service providers: Financial services providers should provide clear, accurate, reliable, comparable, easily accessible, and timely written information on the financial products and services being offered

- Status of recognition by different countries:

- Countries such as the UK and New Zealand have introduced guidelines to identify and provide fair treatment to “vulnerable financial consumers”.

- However, India currently does not recognise this concept, thus regulators such as SEBI prescribe certain financial service providers to assess customer suitability and undertake risk profiling before providing services

- However, amidst challenges like financial illiteracy and economic hardship, it may be worth considering.

Incorporating digitalization in FCP

- Need:

- Technological advancements: FCP must factor in the impact, opportunities and risks of digitalisation for financial consumers amidst increasing number of digital channels and greater use of artificial intelligence, machine learning technology and algorithms.

- Grievance redressal: With the rising number of UPI transactions, concerns regarding redress of grievances against payment service providers and the largely unregulated status of cryptocurrencies

- Case of India - RBI guidelines on digital lending: These guidelines mandated entities providing digital lending services to have a grievance redress officer, assess a borrower’s creditworthiness before extending credit, and allow a borrower to exit without penalty.

Sustainable finance by FCP

- ESG inclusion in finance: Amid growing consumer demand for sustainable financial investments, the financial services providers are incorporating environmental, social and governance (ESG) factors into their operations, products and services.

- However, the FCP recommends improved transparency related to impact, opportunities and risks of sustainable finance for financial consumers to help consumers make informed choices.

- India’s scenario: SEBI has transitioned from “business responsibility reporting” to “business responsibility and sustainability reporting” (BRSR) to promote responsible corporate governance vis-a-vis climate change.

- Compulsory reporting: Eligible companies under BRSR must provide ESG related disclosures, including a sustainability performance report.

- This allows investors to make an informed decision and similar disclosures must be introduced in other market segments.

- Concerns regarding “greenwashing”: This was also highlighted in an expert report presented at COP27.

About Greenwashing

- Definition: Greenwashing is the practice of making false claims in order to mislead consumers into believing that a company's products are more environmentally friendly or have a higher positive environmental impact than they actually do.

- Associated risks: As many of these claims are unverifiable, dubious and may help in boosting the image of the entity and garner benefits for it, it paves way for pushing the world towards climate disaster.

- Examples: The Volkswagen scandal, in which the German car company was found to have been cheating in emissions testing of its supposedly green diesel vehicles, was a case of greenwashing.

- Prevention: Financial regulators must monitor that corporations are not misleading consumers with false claims regarding progress towards climate targets.

Conclusion

- The current regulatory landscape is sectoral and fragmented, resulting in regulatory arbitrage.

- All actors seeking to innovate and compete in FinTech, including incumbent banks, FinTech start-ups and BigTech corporations, should be subject to the same regulatory constraints and oversight.

- Hence, it is necessary to design an effective regulatory regime to prevent the emergence of regulatory gaps that might arise from appearance of new service providers, innovative products, etc.

- An increasing number of people are entering financial markets (as highlighted in RBI’s financial inclusion index) adoption of revised FCP might be a good option.