Unauthorised online lending apps high on FSDC scanner

22-02-2024

01:22 PM

1 min read

What’s in today’s article?

- Why in news?

- What is Financial Stability and Development Council (FSDC)?

- What is Digital Lending?

- Need to regulate digital lending

- Steps taken by to regulate digital lending

- News Summary: Unauthorised online lending apps high on FSDC scanner

Why in news?

- Addressing the 28th meeting of the Financial Stability and Development Council (FSDC), Finance Minister asked financial sector regulators to take further measures to check spread of unauthorised lending through online apps.

Financial Stability and Development Council (FSDC)

- About:

- It is an apex-level body constituted by the Government of India (not a statutory body) in 2010.

- It has been established under the Financial Stability Division of the Department of Economic Affairs (DEA), Ministry of Finance.

- Background:

- Following the global financial crisis of 2008, governments and organisations all over the world were under pressure to regulate their economic assets.

- In 2008, the Raghuram Rajan Committee first advocated the creation of a super regulatory autonomous entity to deal with macro prudential and financial irregularities in India's entire financial system in 2008.

- As a result, the FSDC is considered as India's endeavour to better prepare for future events.

- Composition:

- Chairperson: The Union Finance Minister of India. The Chairperson may invite any person whose presence is deemed necessary for any of its meetings.

- Members:

- Governor Reserve Bank of India (RBl),

- Finance Secretary and/or Secretary, Department of Economic Affairs (DEA),

- Secretary, Department of Financial Services (DFS),

- Secretary, Ministry of Corporate Affairs,

- Secretary, Ministry of Electronics and Information Technology,

- Chief Economic Advisor, Ministry of Finance,

- Chairmans of regulatory bodies like Securities and Exchange Board of India (SEBI), Insurance Regulatory and Development Authority (IRDA), Pension Fund Regulatory and Development Authority (PFRDA), Insolvency and Bankruptcy Board of India (IBBI).

- Secretary of the Council: Additional Secretary, DEA, Ministry of Finance.

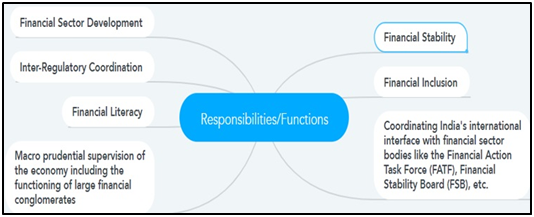

- Responsibilities or functions: There are no funds set aside for the council to carry out its duties.

- Concern and way ahead:

- Because FSDC is led by the Union Finance Minister, the authority of the RBI and other regulators is feared to be jeopardised.

- As a result, the autonomy of sectoral regulators must be safeguarded and functional guidelines must be designed to handle this issue.

What is Digital Lending?

- Digital lending is the process of availing credit online.

- It involves lending through web platforms or mobile apps, utilising technology in customer acquisition, credit assessment, loan approval, disbursement, recovery and associated customer service.

- Its increased popularity amongst new-age lenders can be attributed to expanding smartphone penetration, credit range flexibility and speedy online transactions.

- It includes products like Buy Now, Pay Later (BNPL), which is a financing option (or simply a short-term loan product).

- BNPL allows one to buy a product or avail a service without having to worry about paying for it immediately.

Need to regulate digital lending

- Illegal lending apps in India

- A report by the RBI, published in 2022, says that India has the maximum number of digital loan apps in the world.

- The report has marked 600 loan apps illegal and said that the central bank.

- Low-income and financial unsavvy Indians are the targets

- These apps mostly lend small sums between Rs 2,000 and Rs 10,000, targeting low-income and financial unsavvy Indians.

- These loans come with huge interest rates and extortionate terms and conditions, to which borrowers have no recourse.

- This increases the vulnerabilities of these borrowers by exploiting the unmet need for credit.

- Harassment by recovery agents

- Such apps are dangerous as the harassment by recovery agents have driven many to suicide in the recent past.

- In 2021, at least six people committed suicide in Hyderabad alone due to harassment by agents.

- Such apps are dangerous as the harassment by recovery agents have driven many to suicide in the recent past.

- Breach of privacy

- With just one tap, borrowers allow these lenders to access everything on their phone. The lender also get access to information such as PAN and Aadhar details.

- The apps, on the pretext of advancing a loan, obtain all information from the customers' phones which could later be used by the company to perpetrate some other financial crime.

- Acts as a tool for money laundering

- More than a hundred apps related to loans, betting and dating successfully collected thousands of crores in revenue and repatriated them to China.

- This was revealed an investigation conducted by the Enforcement Directorate (ED).

Steps taken by to regulate digital lending

- RBI has been designated as the nodal department for dealing with complaints against unauthorised digital lending platforms as well as mobile apps.

- In August 2022, RBI issued the first set of guidelines for digital lending in order to combat illegal activities by certain players.

- These guidelines were issued in response to the recommendation of the Working Group on Digital Lending (WGDL).

- In September 2023, Union Finance Minister chaired a meeting with appropriate officials and launched a multi-agency crackdown on illegal loan apps.

- To curb the menace of illegal loan apps, the RBI has been asked to prepare a ‘whitelist’ of legal loan apps.

- At the same time, MEITY has been tasked with ensuring only such legal applications (list prepared by RBI) are available on app stores.

- The RBI has been entrusted to ensure that the registration of payment aggregators be completed within a time frame.

- A payment aggregator acts as a third party responsible for managing and processing merchants' online transactions.

- The RBI has also been entrusted with monitoring ‘mule or rented’ accounts that may be used for money laundering.

- RBI has further been asked to review and cancel dormant non-banking finance companies (NBFCs) to avoid their misuse by such app operators.

- To curb the menace of illegal loan apps, the RBI has been asked to prepare a ‘whitelist’ of legal loan apps.

- The government in December 2023 informed Parliament that Google has suspended or removed over 2,500 fraudulent loan apps from its Play Store between April 2021 and July 2022.

News Summary: Unauthorised online lending apps high on FSDC scanner

- FSDC, chaired by Finance Minister Nirmala Sitharaman, discussed the issue of unauthorised online lending apps’ operations.

- The FSDC deliberated on issues related to macro financial stability and India’s preparedness to deal with them.

- During this, the FM asked the regulators (including the RBI) to take further measures to check spread of unauthorised lending through online apps.

- She also asked regulators to maintain constant vigil and be proactive towards detecting emerging financial stability risks, given the domestic and global macro-financial situation.

Q1) What is Buy Now, Pay Later (BNPL)?

Buy now, pay later (BNPL) is a short-term financing option that lets consumers make purchases and pay for them in installments over time. BNPL is similar to an installment plan money lending process that involves consumers, financiers, and merchants.

Q2) What is the working group on digital lending?

The Government today said that the Reserve Bank of India (RBI) had constituted a working group on digital lending including lending through online platforms and mobile apps.

Source: Unauthorised online lending apps high on FSDC scanner | PIB | Financial Express