Remission of Duties and Taxes on Exported Products (RoDTEP) Scheme

23-01-2024

09:25 AM

1 min read

What’s in Today’s Article?

- Why in News?

- What is the Remission of Duties and Taxes on Exported Products (RoDTEP) Scheme?

- Need for the RoDTEP Scheme

- Features of the RoDTEP Scheme

- Eligibility to Obtain Benefits of the RoDTEP Scheme

- Issues in the Implementation of the RoDTEP Scheme

Why in News?

- The Centre has no plans of re-working the popular Remission of Duties and Taxes on Exported Products (RoDTEP) scheme for exporters, despite the US government imposing anti-subsidy duties against it.

- This is because the issue was not with the WTO compatibility of the scheme but with the inability of exporters to provide adequate documents to US investigating teams.

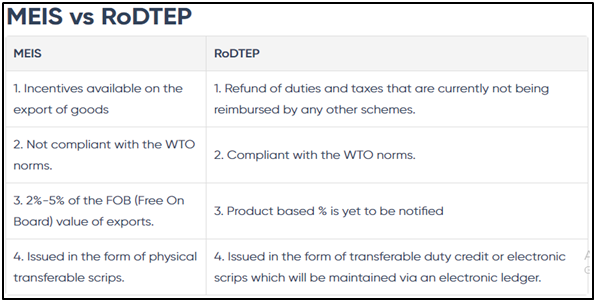

What is the Remission of Duties and Taxes on Exported Products (RoDTEP) Scheme?

- It is a new scheme applicable from 1 January 2021 and is launched by the Ministry of Commerce & Industry to replace the existing MEIS (Merchandise Exports from India Scheme).

- The scheme ensures that the exporters receive the refunds on the embedded taxes and duties previously non-recoverable.

- It was introduced with the intention to boost exports which were relatively poor in volume previously.

Need for the RoDTEP Scheme

- The US had challenged India’s key export subsidy schemes in the WTO (World Trade Organisation), claiming them to harm the American workers.

- A dispute panel in the WTO ruled against India, stating that the export subsidy programmes that were provided by the Government of India violated the provisions of the trade body’s norms.

- The panel further recommended that the export subsidy programmes (like the MEIS, Export Oriented Units Scheme, SEZ Scheme, Duty-Free Imports for Exporters Scheme, etc.) be withdrawn.

- This led to the birth of the RoDTEP Scheme, so as to ensure that India stays WTO-compliant.

Features of the RoDTEP Scheme

- Refund of the previously non-refundable duties and taxes: Mandi tax, VAT, Coal cess, Central Excise duty on fuel, etc., will now be refunded under this particular scheme.

- Automated system of credit: The rebate is issued as a transferable electronic scrip by the Central Board of Indirect Taxes & Customs (CBIC) in an end-to-end IT environment.

- Quick verification through digitisation.

- Multi-sector scheme: Under RoDTEP, all sectors, including the textiles sector, are covered, so as to ensure uniformity across all areas.

- Labor-intensive sectors that enjoy benefits under the MEIS Scheme will be given a priority.

Eligibility to Obtain Benefits of the RoDTEP Scheme

- Manufacturer exporters and merchant exporters (traders) are both eligible for the benefits of this scheme.

- The exported products need to have the country of origin as India.

- There is no particular turnover threshold to claim the RoDTEP.

- The Special Economic Zone Units and Export Oriented Units are also eligible to claim the benefits under this scheme.

- Where goods have been exported via courier through e-commerce platforms, the RoDTEP scheme applies to them as well.

- However, the re-exported products are not eligible under this scheme.

Issues in the Implementation of the RoDTEP Scheme

- RoDTEP is based on the globally accepted principle that taxes and duties should not be exported, and taxes and levies borne on the exported products should be either exempted or remitted to exporters.

- However, both the US and the EU imposed countervailing (anti-subsidy) duties on Indian products, against RoDTEP payments availed.

- The problem is that while the plants have records of total payments made by them in the form of input taxes, they may not have the details.

- For instance, in a hand-written fuel bill given by a petrol pump, it may not give disaggregated Central excise duty and State VAT charges.

- All this needs to be streamlined and the exporters need to be properly trained.

Q1) What is the Central Board of Indirect Taxes & Customs (CBIC)?

CBIC is a statutory body formed in 1964 as the CBEC (Excise) and renamed as the CBIC in 2018. It is a part of the Department of Revenue under the Ministry of Finance, GoI. It deals with the tasks of formulation of policy concerning levy and collection of Customs, Central Excise duties, CGST and IGST, etc.

Q2) What is the Export Oriented Units Scheme?

The Export Oriented Units (EOU) scheme was introduced to boost exports, increase foreign earnings and create employment in India. The EOU scheme is complementary to the scheme for Free Trade Zone, Export Processing Zone.

Source: Centre not to re-work RoDTEP scheme as it is WTO compliant, say officials | PIB