What’s in today’s article?

- About SGB Scheme (Background, Meaning, Working, Benefits, Criticism)

Why in News?

- The Reserve Bank of India (RBI) has announced the Sovereign Gold Bond Scheme 2022-23 – Series III, which will be open for subscription during December 19-23, 2022.

- The issuance price of the Bond during the subscription period will be Rs 5,409 per gram.

What is Sovereign Gold Bond Scheme?

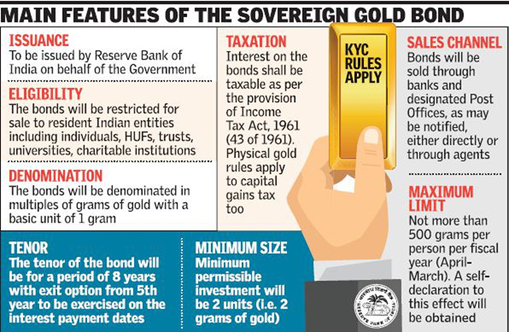

- Sovereign Gold Bonds or SGBs are government securities issued by the RBI on behalf of the Government of India.

- SGBs are denominated in grams of gold. They are substitutes for holding physical gold.

- Investors have to pay the issue price in cash and the bonds will be redeemed in cash on maturity.

How does the Scheme work?

Image Caption: Features of Sovereign Gold Bond Scheme

- SGBs were introduced by the Government of India in 2015 under the Gold Monetization Scheme.

- They are issued by the RBI in different tranches during a financial year.

- These securities are made available via banks, brokers, post offices and online platforms.

- A discount of INR 50 per gram is offered to investors who purchase them digitally to promote buying SGBs online.

- Investors can either buy the bonds in physical, digital or dematerialized format.

- SGBs have a term of eight years and an interest rate of 2.5% per annum paid on a half-yearly basis.

- On maturity i.e. after 8 years, the Gold Bonds shall be redeemed in Indian Rupees and the redemption price shall be based on simple average of closing price of gold of previous 3 business days.

- Early encashment/redemption of the bond is allowed after fifth year from the date of issue on coupon payment dates.

- Every individual purchase is restricted to a maximum of 4kgs per financial year and in case of a trust, it is restricted to 20kgs.

- The only document mandatory for the purchase of SGBs is a PAN card without which no investment in these bonds is permitted.

What are the benefits of SGB?

- The quantity of gold for which the investor pays is protected, since he receives the ongoing market price at the time of redemption/ premature redemption.

- The SGB offers a superior alternative to holding gold in physical form as the risks and costs of storage are eliminated.

- Investors are assured of the market value of gold at the time of maturity and periodical interest.

- SGB is free from issues like making charges and purity in the case of gold in jewellery form.

- The bonds are held in the books of the RBI or in demat form eliminating risk of loss of script etc.

- SGBs are eligible to be used as collateral for loans from banks, financial Institutions and Non-Banking Financial Companies (NBFC).

- The bonds are tradable from a date to be notified by RBI. The bonds can also be sold and transferred as per provisions of Government Securities Act, 2006.

What is the criticism of Sovereign Gold Bond Scheme?

- Maturity Period –

- A lot of investors are discouraged by the gold bonds because of long maturity period of 8 years.

- The government has kept the maturity long in order to prevent gold price volatility resulting in losses for the investors.

- Risk of Capital Loss –

- Investment in SGB can result in a capital loss as the bond value is directly linked to the price of gold in the international markets.

- If the price at which you buy the bond is higher than the price at which you redeem it at maturity, you might end up in a loss.

Performance of the scheme

- The government has issued gold bonds for 96,283 kg (96.28 tonnes) in 61 issuances since 2016-17, which is worth Rs 52,080 crore at the current market price.

- Investors have made premature redemption of 876 kg of gold bonds so far.

Q1) What is the maturity period of Sovereign Gold Bond?

SGBs have a term of eight years and an interest rate of 2.5% per annum paid on a half-yearly basis.

Q2) What is the meaning of dematerialised format?

Dematerialisation is a process through which physical securities such as share certificates and other documents are converted into electronic format and held in a Demat Account.

Source: Sovereign Gold Bonds, a substitute for physical gold

![]() Last updated on June, 2026

Last updated on June, 2026

→ UPSC Prelims Provisional Answer Key 2026 out for GS Paper 1 and CSAT.

→ UPSC Prelims Question Paper 2026 Out, Download GS Paper 1 PDF conducted on 24th May 2026.

→ UPSC Mains 2026 will be conducted from 21st August 2026 onwards, and UPSC Prelims 2027 will be held on 23rd May 2027.

→ Prepare effectively with Vajiram & Ravi’s UPSC Prelims Test Series 2027 featuring full-length mock tests, detailed solutions, and performance analysis.

→ UPSC Final Result 2025 is now out.

→ UPSC has released UPSC Toppers List 2025 with the Civil Services final result on its official website.

→ Anuj Agnihotri secured AIR 1 in the UPSC Civil Services Examination 2025.

→ UPSC Notification 2026 & UPSC IFoS Notification 2026 is now out on the official website at upsconline.nic.in.

→ UPSC Calendar 2027 has been released.

→ Check out the latest UPSC Syllabus 2026 here.

→ The UPSC Selection Process is of 3 stages-Prelims, Mains and Interview.

→ Enroll in Vajiram & Ravi’s UPSC Mains Test Series 2026 for structured answer writing practice, expert evaluation, and exam-oriented feedback.

→ Join Vajiram & Ravi’s Best UPSC Mentorship Program for personalized guidance, strategy planning, and one-to-one support from experienced mentors.

→ Shakti Dubey secures AIR 1 in UPSC CSE Exam 2024.

→ Also check Best UPSC Coaching in India